Choosing a payment gateway UAE merchants can rely on isn’t just technical—it directly impacts revenue. UAE shoppers expect fast mobile payments, strong card acceptance, smooth refunds, and clear security.

If your online payment processing is slow, unreliable, or missing key methods, conversion drops and chargeback risk rises.

This guide explains how to choose the right gateway for your business model, handle payment gateway integration beyond “install a plugin,” and secure ecommerce payments without adding friction.

Message Lucidly on WhatsApp for a quick payment setup review.

Start with the UAE context before you choose

When comparing payment gateways UAE providers, anchor on the realities that affect success here:

Regulation and licensing matter. The Central Bank of the UAE (CBUAE) sets a regulatory framework for retail payment services and card schemes, focusing on safety, efficiency, and confidence in payment transactions.

Data protection is part of your responsibility. The UAE has a federal Personal Data Protection Law framework (PDPL) to protect confidentiality and privacy and define governance for data management.

Security expectations are high. Card authentication (like 3D Secure) and strong security controls influence approval rates, fraud, and customer trust.

This is why “the cheapest provider” often becomes the most expensive over time—through failed payments, poor reporting, dispute losses, and operational overhead.

How to choose a payment gateway in the UAE (decision framework)

A good online payment gateway UAE setup is the one that matches your model, reduces payment friction, and protects you from avoidable risk.

A) Match the gateway to your business model

Ask these first:

Standard ecommerce store: You need strong card acceptance, wallets, fast refunds, and easy reconciliation.

Subscriptions / memberships: You need tokenization and recurring payment support (plus solid dunning/failed payment handling).

Marketplaces: You may need split payments, sub-merchants, payouts, and higher compliance complexity.

High-ticket / B2B invoices: You may benefit from pay-by-link and bank transfer options alongside card payments.

This helps you avoid a gateway that looks “feature-rich” but can’t actually support your revenue mechanics.

B) Confirm core capabilities (the non-negotiables)

When shortlisting a payment gateway UAE option, verify these capabilities clearly:

AED settlement (and multi-currency if you sell cross-border)

Partial refunds and flexible refund workflows

Chargeback handling and evidence support

3D Secure (3DS2) support and configuration options

Clear reporting for transaction fees, authorization rates, and payout schedules

Also check operational details that rarely appear on pricing pages:

Support quality (response time, technical support depth)

Dashboard clarity (finance teams need usable exports)

Reliability and latency (especially on mobile)

C) Understand total cost (not just headline fees)

Most merchants compare only the per-transaction fee. You should calculate:

Transaction fees (MDR / per-transaction charges)

Refund fees (some providers charge for processing refunds)

Chargeback fees

FX fees for cross-border or multi-currency settlement

Monthly minimums or maintenance costs

Settlement timelines (cashflow impact)

A slightly higher fee can be worth it if your approval rate is higher and your failures are lower—because that increases completed orders.

D) Payment processor vs gateway (why it matters)

Many merchants mix terms. A “gateway” often routes and authenticates payment data, while a “processor/acquirer” handles the actual card transaction flow and settlement.

In practice, many providers bundle these roles—but when troubleshooting, pricing, or negotiating, it helps to understand payment processor vs gateway so you know who controls approvals, declines, and payout terms.

If you want to strengthen your store setup before choosing a gateway, read our guide to building an Ecommerce Website Development in the UAE that sells.

Payment gateway integration in the real world

A clean payment gateway integration is not “installed and done.” It’s a controlled flow that keeps orders consistent, inventory accurate, and payment events tracked.

A) Choose the integration type: Hosted vs embedded vs API

Hosted checkout (redirect or hosted payment page): Faster to launch, reduces PCI scope, often best for SMEs.

Embedded fields / payment elements: Better UX control, but requires careful implementation and security.

Full API integration: Most flexible (subscriptions, advanced flows), but highest engineering responsibility.

If you’re optimizing for speed-to-market, hosted is often the safest path. If you’re optimizing for full control and unique flows, API becomes valuable.

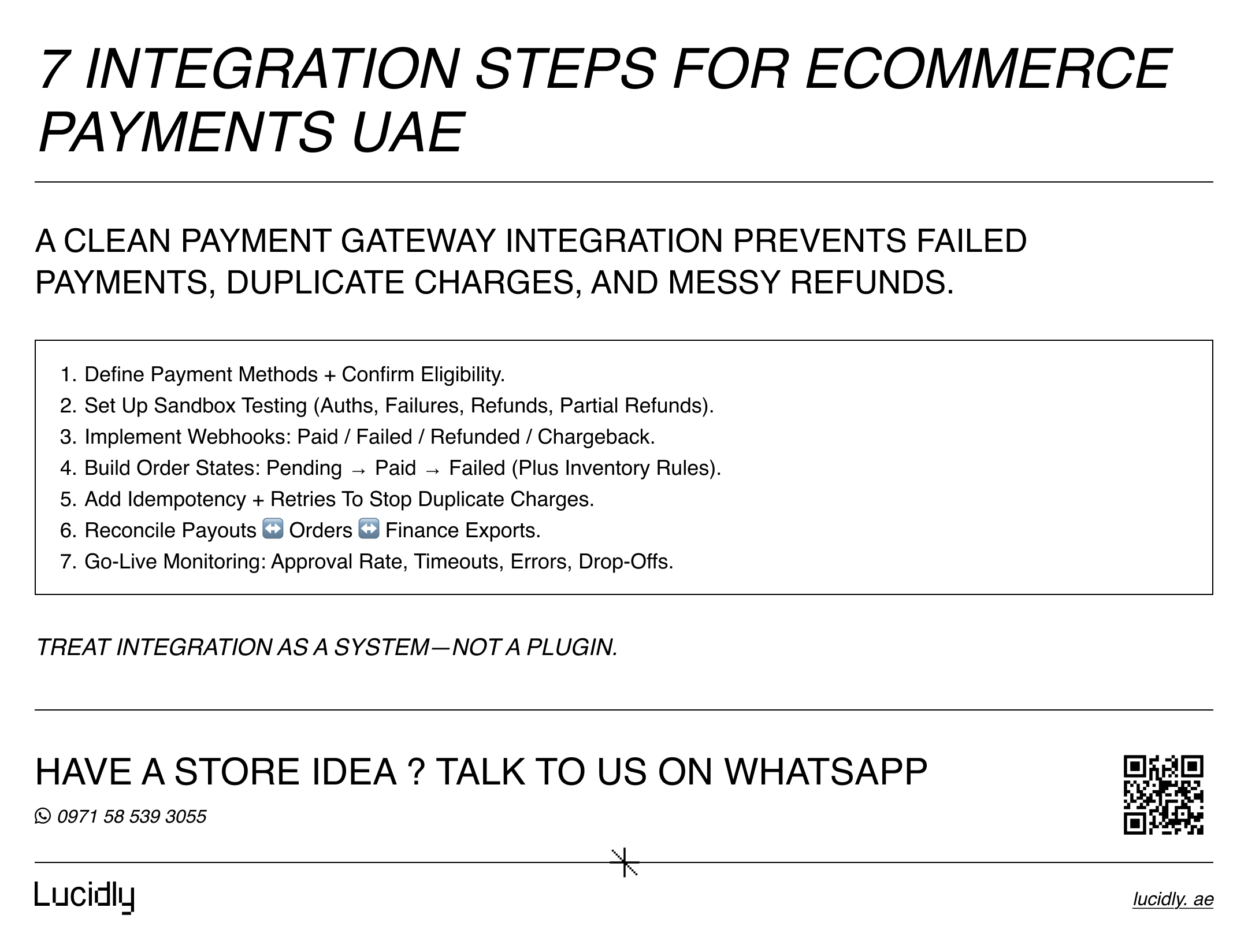

B) The integration checklist (what good teams actually do)

Here are 7 integration steps for ecommerce payments UAE:

Define payment methods (cards, Apple Pay/Google Pay if relevant, BNPL if needed) and confirm eligibility.

Set up sandbox/testing: test authorizations, failed payments, refunds, partial refunds.

Implement webhooks (or equivalent callbacks) for:

paid / failed / refunded / chargeback events

Design order state logic:

“Payment pending” vs “Paid” vs “Failed”

inventory reservation rules

Add idempotency and retry strategy:

prevent duplicate charges when users refresh or timeouts happen

Reconciliation flow:

gateway payouts ↔ store orders ↔ finance/accounting exports

Go-live monitoring:

authorization rate, timeouts, error messages, drop-offs by step

This is the difference between “it works on launch day” and “it works under real traffic.”

C) UAE-specific integration pitfalls to avoid

For payment gateway UAE implementations, watch these common pitfalls:

Launching without clear refund flows (refunds are a trust lever)

Weak chargeback evidence capture (delivery proof, order logs, communications)

Not tracking payment failures by reason (issuer declines vs gateway errors)

Ignoring mobile latency (a few seconds can drop conversions)

If you want to reduce checkout friction and recover more completed orders, explore our guide to ecommerce checkout optimisation.

If you want to reduce checkout friction and recover more completed orders, explore our guide to ecommerce checkout optimisation.

How to keep payments secure (without killing conversion)

Security isn’t only about preventing fraud—it’s also about avoiding operational disasters and reducing dispute exposure.

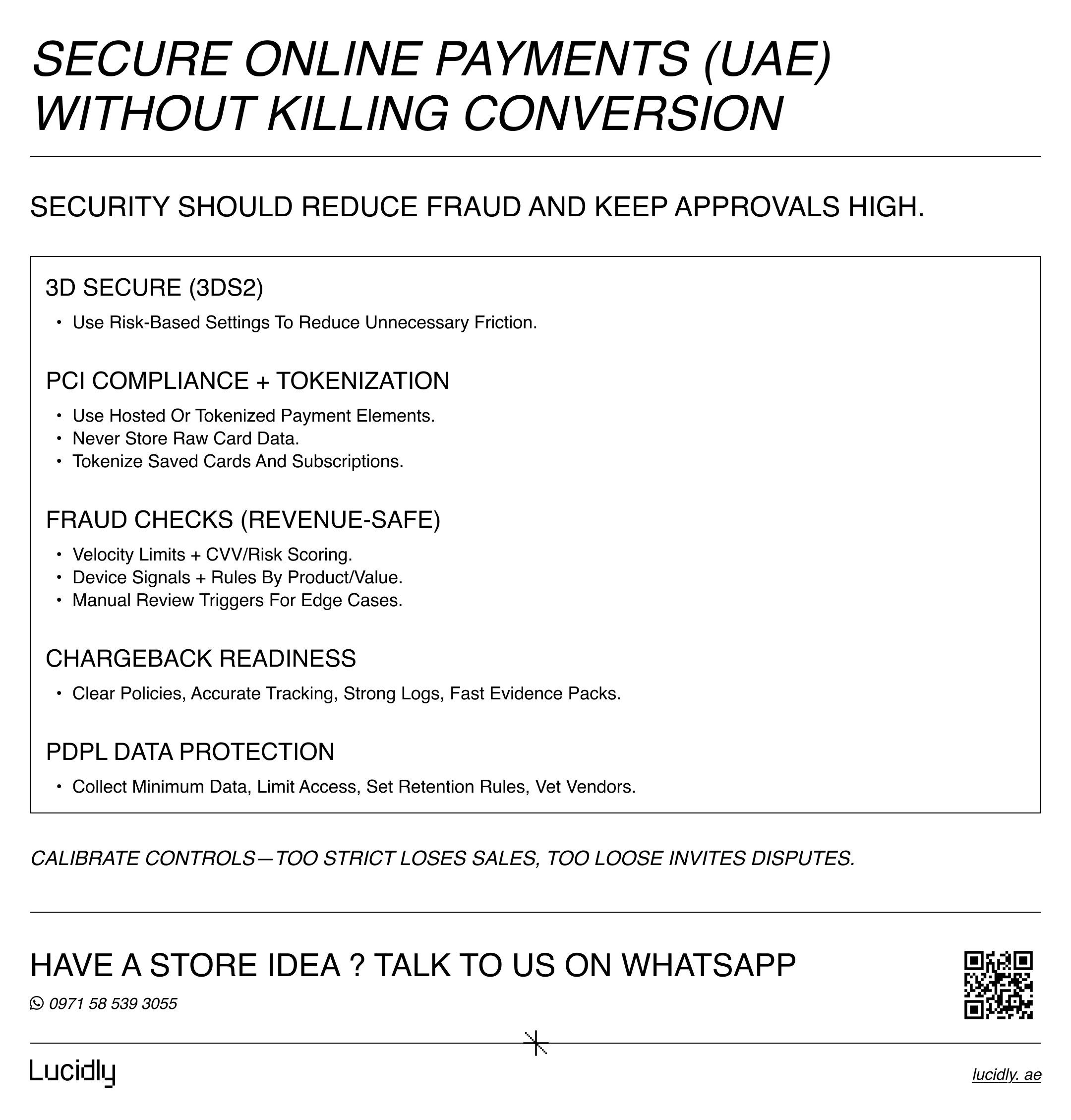

A) Use 3D Secure the smart way

3D Secure (3DS2) is the industry standard for cardholder authentication. In many cases, it can reduce fraud and shift liability depending on scheme rules, but implementation quality matters. Use risk-based settings where possible so low-risk users aren’t forced into unnecessary friction.

B) Reduce PCI scope with tokenization and safer architectures

If you can avoid handling raw card data, do it. PCI Security Standards Council guidance explains tokenization and how it can affect PCI DSS scope.

Practical steps:

Prefer hosted payment pages or tokenized payment elements.

Never store raw card numbers on your servers.

Use tokenization for saved cards and recurring billing.

This improves security posture and reduces your PCI compliance burden by keeping sensitive card data out of your systems.

C) Fraud checks that protect revenue (not just block orders)

Strong fraud checks should be layered and measurable:

Velocity rules (too many attempts per user/device/IP).

CVV checks and risk scoring (based on gateway support).

Device fingerprinting / behavioral signals (if available).

Rules by product category and order value.

Manual review triggers for edge cases.

The key is calibration: too strict, and you lose good orders; too loose, and you invite fraud and chargebacks.

D) Build a chargeback-ready operation

Chargebacks are part of online payment processing. Your job is to reduce them and win more disputes:

Make shipping/returns policies clear at checkout.

Send accurate order confirmations and tracking.

Store logs: timestamps, IP/device signals, delivery proof.

Respond fast with a structured evidence pack.

In the UAE market (especially for high-ticket or fast-moving categories), chargeback readiness can be the difference between stable scaling and constant firefighting.

E) Align with UAE data protection expectations

Even if you’re not storing card data, you still handle personal data (names, phone numbers, addresses, emails). The UAE PDPL framework is designed to protect confidentiality and privacy and establish governance for data management.

Practical approach:

Collect only what you need.

Control access internally (least privilege).

Set retention rules (don’t keep data forever “just in case”).

Ensure vendors meet your security requirements.

These steps help any payment gateway UAE setup stay secure while preserving conversion.

For a performance-first payment setup, explore Lucidly’s Ecommerce Solutions in the UAE to choose, integrate, and secure the right gateway for your store.

If you want a broader view of payment security, fraud prevention, and customer data protection, read our ecommerce security guide.

Quick shortlist scorecard (use this to decide)

When selecting a payment gateway UAE provider, score candidates on:

Authorization rate (real approvals, not marketing claims)

Total cost (fees + refunds + chargebacks + FX)

Settlement speed and clarity

Integration effort (plugins vs API, webhook quality)

Security features (3D Secure, tokenization, anti-fraud tools)

Reporting and reconciliation

Support quality (technical + operational)

This approach is more reliable than picking based on a top-10 list.

FAQ

What is a payment gateway?

A payment gateway is the technology that helps your store accept digital payments securely by routing transaction data and enabling authentication and authorization. In many setups, the gateway works with a processor/acquirer—hence the importance of understanding payment processor vs gateway when diagnosing declines or payout issues.

Which payment methods should UAE stores offer?

For ecommerce payments UAE, most stores should at minimum support card payments and fast mobile-friendly checkout options where relevant. The best mix depends on your audience, product type, and average order value—then you test what improves approvals and completion.

How do I integrate a payment gateway?

Start by choosing the integration type (hosted vs embedded vs API), then follow a controlled payment gateway integration checklist: sandbox testing, webhook events, order-state logic, idempotency, reconciliation, and monitoring. This prevents duplicate charges, missing orders, and refund confusion.

How do I keep payments secure?

Use 3D Secure (3DS2) appropriately, reduce PCI exposure by using hosted/tokenized approaches, implement layered fraud checks, and prepare for chargebacks with strong evidence collection. Tokenization guidance from the PCI SSC is a useful reference for reducing risk and scope.

The right payment gateway UAE improves approval rates, fits your business model, and stays secure under real traffic. Treat integration as a system (not a plugin) and protect payments with 3D Secure, tokenization, and calibrated fraud checks.

Ready to upgrade your online payment gateway in the UAE and boost checkout conversions? Message Lucidly on WhatsApp—or use the numbers on our Contact Us page to book a quick payment review.

References

Central Bank of the UAE (CBUAE) Rulebook — Retail Payment Services and Card Schemes Regulation. (Rulebook)

The Official UAE Government Portal (u.ae) — Data protection laws (UAE PDPL overview). (U.ae)

UAE Legislation Portal — Federal Decree-Law No. (45) of 2021 Concerning the Protection of Personal Data (PDPL) (official text download). (UAE Legislation)